Just recently, the Budget 2024 speech by Deputy Prime Minister Lawrence Wong announced the closure of CPF Special Accounts (SA) for those aged 55 and above.

As a result, from 2025, those aged 55 and above will only have three CPF accounts – Ordinary Account (OA), Retirement Account (RA), and MediSave Account (MA).

Those under 55 will still retain their SA, and will also have a total of three CPF accounts – OA, SA, and MA (without RA, of course).

You’ve probably heard lots of people talking about the CPF changes, but you may not even know what these accounts are.

Reader: Isn’t CPF just CPF? All the same what, no meh?

There’s actually a difference in many things like interest rate, whether or not you can withdraw, and more.

Read on to learn all about CPF Special Account so you won’t be that one person who needs everything explained to them when your friends talk about it.

The Different CPF Accounts

At the start of your career, 20% of your total monthly wages goes into your CPF account and your employer contributes an additional 17%.

This 17% is not part of your total monthly wages.

If you are a Singaporean citizen aged 35 and below, 37% of your total monthly wages (i.e. total CPF contribution) will be allocated to your CPF Ordinary Account (23%), MediSave Account (8%), and Special Account (6%).

The CPF Ordinary Account (OA) supports your home purchase.

The CPF MediSave Account (MA) helps pay for certain medical expenses.

The CPF Special Account (SA) accumulates savings for your retirement.

As you grow older and near retirement age, the SA percentage slowly increases to 11.5%, putting a focus on your retirement savings when you’re between 50 and 55.

At the same time, contributions to your MA also increase, while contributions to your OA slowly decrease.

When you turn 55 years old, a CPF Retirement Account (RA) is automatically created. Your savings from your SA and OA, up to the current FRS, will be transferred to your RA to form your retirement sum. This account is meant to provide you with monthly payouts in retirement.

The Reason Behind the Closure of CPF SA

The reason behind the closure of the SA for those above 55 is actually very simple.

First, we have to look at some details of the SA.

Because the money in this account is meant for your retirement, it has to be kept very, very safe so you don’t anyhow spend your savings on $200 Louis Vuitton chocolate.

Hence, SA savings cannot be withdrawn until age 55.

On the bright side, you enjoy higher interest rate on savings in your CPF SA (yay!).

However, as a principle, only savings that cannot be withdrawn on demand should earn the long-term interest rate, and savings that can be withdrawn on demand should earn the short-term interest rate.

Since SA gives you higher interest rate, it doesn’t really make sense that you can withdraw it, right?

Sure, it makes you happy because you can withdraw on demand and still enjoy higher interest rate, but it also doesn’t really make sense.

To better align CPF interest rates with the nature of CPF savings in each CPF account, the SA of those aged 55 and above will be closed from early 2025.

But don’t worry, your savings are not going to just vanish into thin air.

The Closure of CPF SA

For those who are still working, the share of your CPF contributions, which would normally go into your SA, will go into your RA instead.

SA savings will be transferred to your RA, up to your Full Retirement Sum (FRS). These savings in your RA will continue to earn the long-term interest rate.

If your SA is bursting – huat ah – and you have leftover savings after meeting the FRS, any remaining SA savings will be transferred to your OA. There, they will remain withdrawable and will earn the short-term interest rate.

If you want to get long-term interest rate on even more savings, you can choose to transfer your OA savings to the RA at any time, up to the prevailing Enhanced Retirement Sum (ERS). Do note that this action cannot be reversed.

Once transferred, RA savings can only be streamed out to you in retirement payouts.

Given that RA savings cannot be withdrawn (except for in the form of monthly payouts), a lot of people feel negatively about this change. With the closure of SA, you’re basically forced to choose between withdrawal flexibility and higher interest rate.

As DPM Lawrence Wong mentioned in his Budget 2024 speech, the ERS will be raised from 1 January 2025, allowing CPF members to receive higher monthly payouts in their retirement.

With the raised ERS, more than 99% of members aged 55 and above today will be able to transfer all their SA savings, that were channeled to the OA due to the closure of SA, to the RA.

What this basically means is that the savings that had previously been enjoying higher interest rate in SA will still be able to enjoy higher interest rate in RA even after the closure of SA.

How This Affects You

Since your SA savings will be transferred to your RA, you will be able to enjoy higher retirement payouts (yay!).

For those who simply use SA as a higher-interest savings account, you won’t really be affected by the closure as your SA savings will continue to earn higher interest rate in your RA.

The biggest impact of the SA closure will be felt by those who have already reached their FRS. Their SA funds and any new contributions will be channeled to their OA, which offers lower interest rate.

This is why lots of people feel strongly about the closure of SA.

To get around this, one can transfer their OA savings to their RA, but as mentioned before, this action cannot be undone.

Those who practise CPF shielding may also be affected.

CPF shielding, or Special Account shielding, refers to investing one’s SA savings through the CPF Investment Scheme to prevent them from being transferred to the RA at 55.

After the RA is created, these people liquidate their investments and keep the funds in their SA to enjoy withdrawal flexibility and higher interest rates.

Once the SA is closed in 2025, any proceeds from the investment will be paid into the RA. If the FRS in the RA is met, the monies will go to the OA instead, where the interest rate is lower.

So no, you won’t be able to enjoy withdrawal flexibility and higher interest rate. You can’t have your cake and eat it too.

If you’re still confused, this video below should help you understand this better with visuals.

So How and When Can I Withdraw CPF?

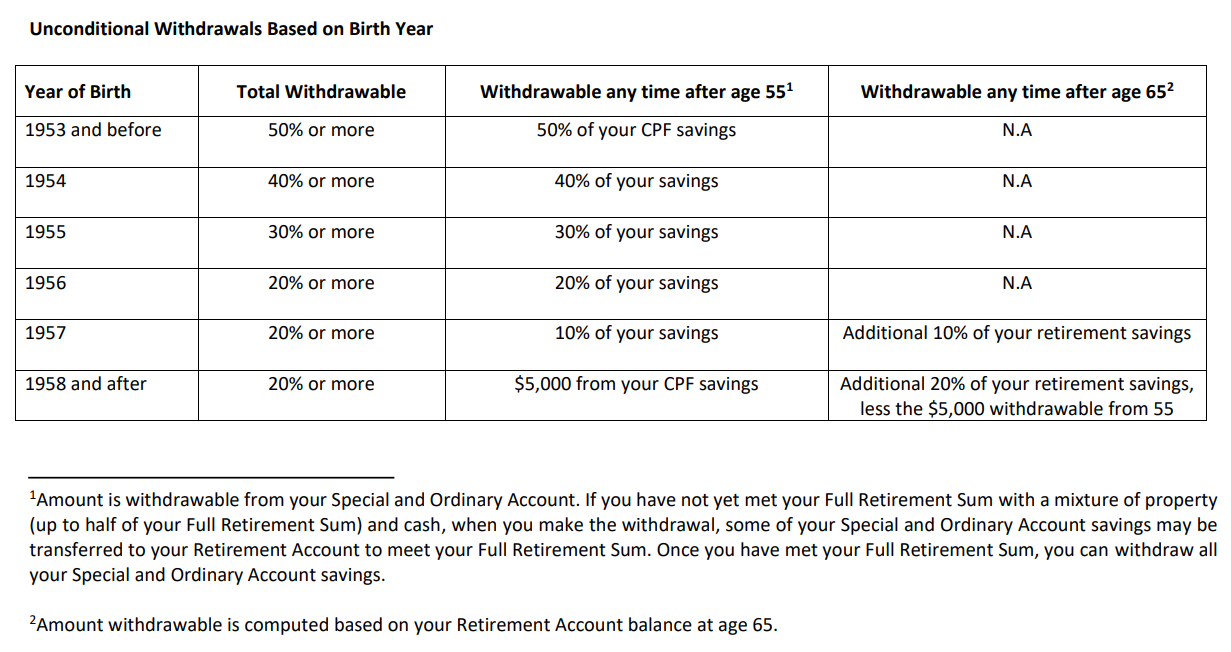

You can start withdrawing your CPF savings from age 55. You don’t need to withdraw everything at one shot, you can withdraw only what you need so that the rest of your savings will remain in the account and continue to earn interest.

When you withdraw CPF savings, you’ll be withdrawing from your OA and SA. Once your SA closes in 2025, you’ll be withdrawing only from your OA.

If you have not yet met your FRS with a mixture of property (up to half of your FRS) and cash, when you make the withdrawal, some of your SA and OA savings may be transferred to your RA to meet your FRS.

Once you have met your FRS, you can withdraw any amount in your SA and OA, you can even withdraw all your SA and OA savings.

Note that the amount you can withdraw depends on your year of birth and the age you are making the withdrawal.

Property owners will be able to access more CPF funds as long as these two conditions are fulfilled:

- The property you own must be in Singapore; and

- the remaining lease on your property must last you up to at least age 95.

Property owners have the flexibility to set aside their FRS with a mixture of property (up to half the FRS, which is the Basic Retirement Sum (BRS)) and cash, and withdraw part of their RA savings down to the BRS.

Do note, however, that withdrawing from your RA will lower your future monthly payouts, so weigh your short- and long-term goals carefully.

I’ve been talking about monthly payouts throughout this article but you may still be wondering how to get these.

In general, you will be automatically included in the CPF LIFE scheme if you were born in 1958 or after, have at least S$60,000 in your RA six months before you reach 65, and are a Singapore Citizen or Permanent Resident.

For those enrolled in CPF LIFE, you’ll get monthly payouts no matter how long you live.

If you somehow live till 200 and the Earth hasn’t died yet, yes, you’ll still be receiving monthly payouts.

There are three plans under CPF LIFE – the Basic Plan, Standard Plan, and Escalated Plan. Under these three plans, your RA savings will be used to pay the premiums for your CPF LIFE plan.

The Basic Plan gives you lower payouts, and about 10-20% of your RA savings is deducted for the CPF LIFE premium. Your monthly payouts will first be paid from your RA and is estimated to last until 90. After that, monthly payouts will be paid from your CPF LIFE premium.

The Standard Plan gives you a stable payout for life, and 100% of your RA savings will be used to pay a lump sum premium when you join.

The Escalating Plan will give you lower initial payouts than the Standard Plan but will increase by 2% yearly. Eventually, it will become higher than payouts in the Standard Plan in the long run. Similar to the Standard Plan, 100% of your RA savings will go into the lump sum premium.

See more details here.

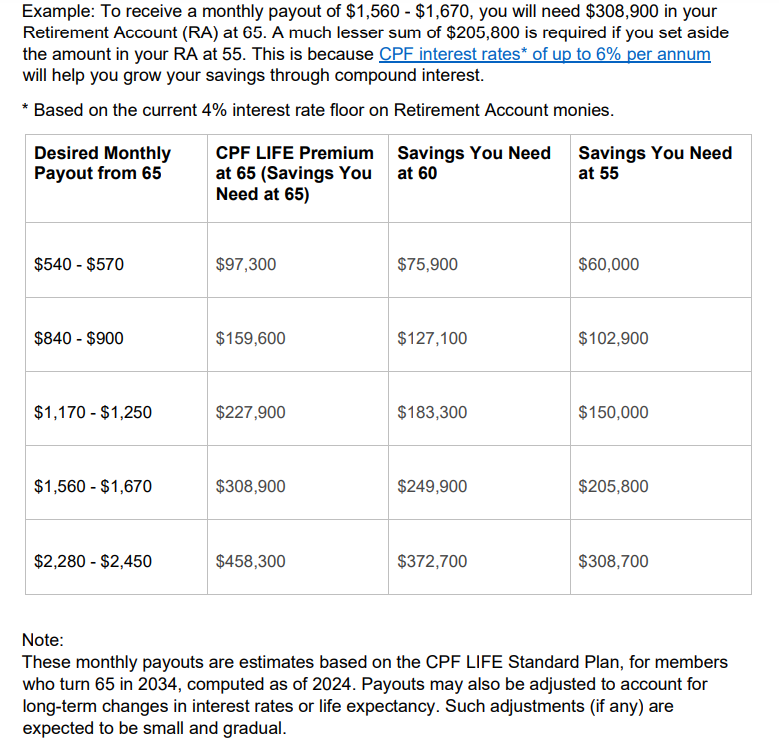

Here’s an example what you’ll need to save to get your desired monthly payout, or what payout you can expect to get based on your savings:

For those who are not eligible for CPF LIFE, you can apply to start receiving monthly payouts from the age of 65. Those who do not do so will automatically start receiving payouts at age 70.

Your monthly payouts are calculated to last for up to 20 years based on the prevailing base interest rate earned on your RA savings when you start your payouts. With an additional interest (up to 2%) paid by the government, you can expect to receive payouts up to age 90, or another five years, whichever is later.

Those not on CPF LIFE can use this payout estimator to estimate the amount of monthly payouts you can receive from your retirement savings.

If you are currently receiving payouts, your payouts will increase due to the transfer of your SA savings to your RA, as mentioned before. You will be notified to check your monthly payouts after the transfer and closure of your SA in early 2025.