Scams, again—with more new variants popping up faster than Don Don Donki outlets, people really need to be careful now, more than ever.

Recently, this woman received $1000 from a scammer and was asked to pay back $1,350 in just five days, despite rejecting his earlier offer of the sum.

Here’s what you need to know.

What Happened

In a story submitted on the website STOMP, a woman with the last name Lim detailed how she got scammed after answering an advertisement offering loans.

On 23 March, she stumbled upon the Whatsapp ad, which caught her eye because she intended to borrow SGD$100,000. The scammers offered this sum with a monthly repayment plan of $1,830 over a period of 60 months, adding up to only $9,800 in interest after five years.

Deciding that this monthly sum was within her means, she decided to reply to the scammer’s message, dubbing him “Ah Boy” in her recount.

This “Ah Boy” then supplied her with his company’s alleged Acra (Accounting and Corporate Regulatory Authority) number, assuring her he was a licensed moneylender.

Trusting him, she made the mistake of divulging her personal details to him through Whatsapp—including her NRIC, payslip, CPF contribution and more, in order to let him “analyse” if the loan was suitable for her.

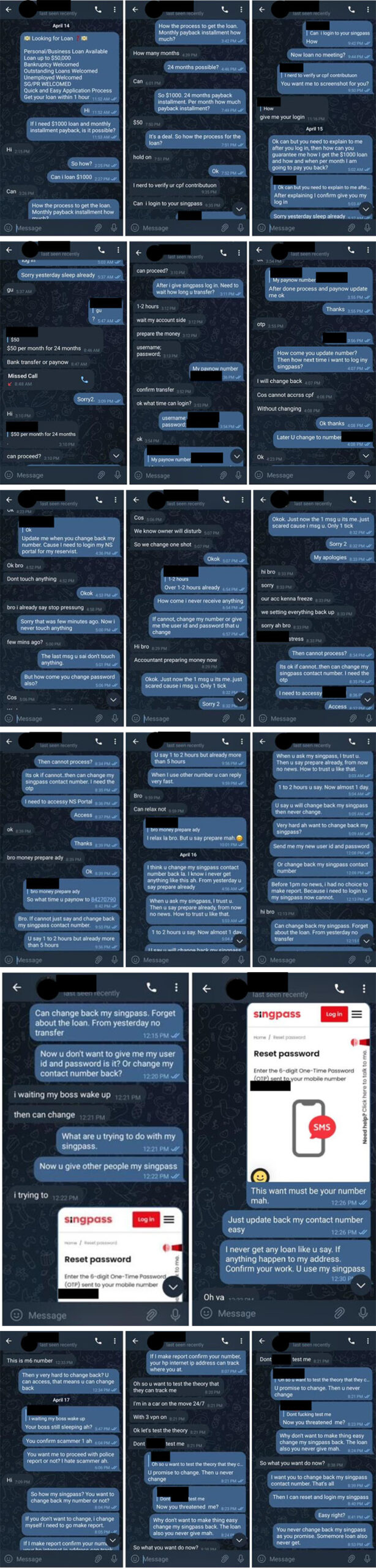

When “Ah Boy” contacted her again, though, she quickly realised it was a scam. He told her he would lend her $1,000, and she had to pay $1,350 back in five days before the $100,000 could be loaned because she’d never taken a loan before.

She attempted to reject this offer, expressing that she was no longer interested, but the “Ah Boy” deposited $1,000 using a cash deposit machine into her bank account, providing her with a loan contract.

Backtracking, she tried to ask him for his account number to return the money, but he refused, citing that the loan had already been processed. Without a way out, she headed to the police station to make a police report.

Investigations are now ongoing.

How Do Loan Scams Work?

In this scam variant, called a loan scam, victims typically receive unsolicited messages about loans through messaging platforms like Telegram or Whatsapp.

Victims who reply to the message would then be asked to provide personal details, usually their Singpass credentials, on the guise of verifying their employment status to approve the loan.

Scammers would then use these credentials provided to try to make bank accounts or sign up for telephone lines. They may also instruct victims to transfer money to bank accounts provided, using the excuse of paying administrative or collateral fees to facilitate the loans.

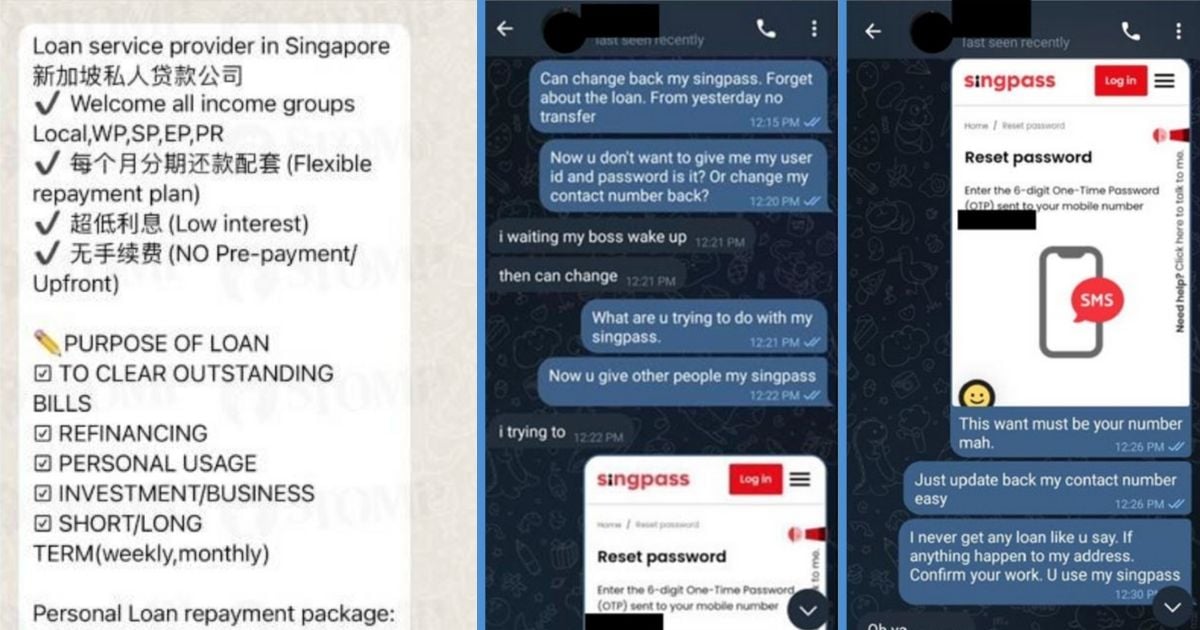

These are screenshots provided by the Singapore Police Force (SPF), showing a conversation with a scammer:

Victims eventually discover they’ve been scammed when they realise they have not and will not receive the loan.

The SPF recommends steps you can take to prevent falling victim to these scams.

According to them, you should ignore those advertising messages and not reply. If you receive that kind of message, block the number and report it as spam, if the messaging platform provides that function.

Also, refrain from providing personal information like Singpass credentials, your NRIC, or your one-time passwords (OTP) to anyone, because it can be used to create bank accounts used for illegal transactions and activity.

Additionally, Singpass contact details should be updated regularly, so users receive updates when important changes have been made, allowing them to quickly secure their account if it’s been compromised.

They also remind the public of a few facts about real licensed moneylenders, who are actually not allowed to solicit loans through text messages, phone calls, or other social media platforms.

Licensed moneylenders also will not ask for CPF contribution details or Singpass login credentials, and are required to meet the borrower in person at their approved place of business. Loan transactions cannot be performed fully online.

The business addresses of all licensed moneylenders in Singapore are published here.

Loan applicants also will not be asked to make any payments before a loan is disbursed, like a “processing fee” or an “administrative fee”, and can only deduct this fee from the loan principal disbursed to the borrower.